High investor demand and moderate economic growth expected to maintain U.S. real estate pricing in 2020

Strong demand from both domestic and foreign investors, combined with moderate economic growth, is expected to keep capitalization rates for U.S. commercial real estate assets broadly stable in 2020, according to the latest research from global property advisor CBRE.

The CBRE North America Cap Rate Survey found that industrial, multifamily, and suburban office cap rates tightened the most in H2 2019, while hotel and retail cap rates were generally unchanged except for a negligible increase for retail power centers. Continued cap rate stability is expected in the first half of 2020 across property types, segments, classes and market tiers, except for a slight increase in the hotel sector.

“U.S. real estate assets remain in high demand from domestic and foreign investors. Cap rates were stable in 2019 and we expect them to remain so in 2020, despite the uncertainty created by the coronavirus and the upcoming presidential election. Continued moderate economic growth will keep interest rates low, and sustain demand for commercial real estate,” said Richard Barkham, global chief economist for CBRE.

Among the major commercial real estate sectors:

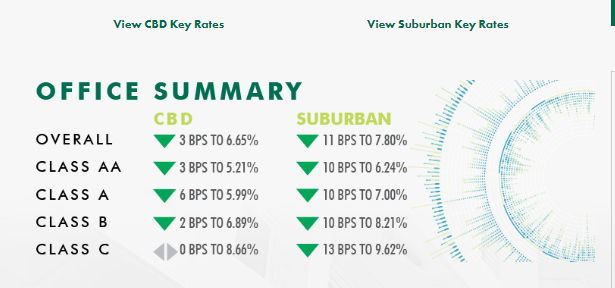

Office: Strong market fundamentals continue to support competitive pricing for office properties. There were minimal changes in office cap rates in H2 2019, continuing a pattern of stability over the past three years and remaining near record-lows for this cycle. Tier II markets, particularly in the suburbs, were one of the few categories with a noticeable downward movement in cap rates. No change in office cap rates is expected in H1 2020.

“Ten years of virtually uninterrupted demand and stable employment growth continue to underpin a favorable and competitive environment for U.S. office properties. Cap rates remain near record lows, supported by cyclically high levels of global and domestic investment capital seeking office assets. Our outlook is for continued cap rate stability for office assets in the first half of 2020,” said Chris Ludeman, global president of Capital Markets for CBRE.

Industrial: Soaring asset values led to sustained cap rate compression in H2 2019. Cap rates are expected to remain broadly stable in 2020, with some moderate tightening. Cap rates for acquisitions of stabilized assets averaged 6.13% for all tiers and classes, falling by 13 bps (basis points) in H2 2019. Rates for value-add acquisitions fell by 17 bps to 7.18%. Class A cap rates declined 10 bps to 4.89%, the lowest level since CBRE’s Cap Rate Survey began in H1 2009.

“Industrial assets remain the most sought-after, dynamic commercial property type. Strong demand from e-commerce, third-party logistics operators, and the food & beverage industry have led to rising asking rents and near all-time low vacancy rates. Continued economic growth will drive supply chain activity across the country and spur demand for logistics real estate in an already supply-constrained environment,” said Jack Fraker, Global Head of Industrial & Logistics for CBRE.

Retail: Cap rates were relatively stable in H2 2019, especially across Tier I and II markets, and Class A and B properties, with few sales of core assets. Tier III markets and Class C assets attracted increased investment activity among private buyers due to higher risk tolerance and opportunities for redevelopment.

“Grocery-anchored neighborhood centers remain the favorite retail asset class for investors because of perceived resilience in a recession and relatively low e-commerce penetration. Store formats that incorporate technology to attract consumers and create demand are particularly attractive to investors,” said Melina Cordero, leader of CBRE’s retail capital markets business for the Americas.

Multifamily: Cap rates and expected returns on cost remained at historically low levels in H2 2019. Cap rates edged down 9 bps to 5.11% for infill stabilized assets and by 11 bps to 5.37% for suburban assets. Cap rate spreads between Class A and Class C assets, and between Tier I and Tier III markets continued to tighten, indicating that many investors are finding opportunities in lower-quality assets and in secondary and tertiary markets.

“Continued healthy market fundamentals—particularly low vacancies and steady rent growth—contributed to multifamily’s appeal and sustained high levels of investment at low cap rates. Low-interest rates contributed to a favorable view of the sector and influenced pricing decisions. There is more optimism for continued solid pricing in H1 2020,” said Brian McAuliffe, leader of CBRE’s multifamily capital markets business for the Americas.

Hotels: Cap rates were essentially unchanged in H2 2019, down by just 1 bp to 8.27%. Cap rates for both CBD and suburban properties were stable. A long-term trend of shrinking cap-rate spreads between market tiers continued in 2019. Spreads between CBD and suburban full- and select-service hotels remained slightly elevated compared with 2018.

“Hotel cap rates are flat despite late-cycle fundamentals weighing on investors. Offsetting sluggish fundamentals is the continued appetite from equity investors for yield, combined with the positive spread between risk-free rates and stabilized yields for the asset class,” said Kevin Mallory, Global Head of CBRE Hotels.