CBRE’s 2021 U.S. Real Estate Outlook: Speed of recovery mixed with quicker rebound for industrial and data centers

CBRE expects that 2021 will see a strengthened recovery of all U.S. commercial real estate sectors as the broader economy bounces back from the pandemic-induced recession and even as a potentially split federal government tempers fiscal stimulus plans.

CBRE anticipates that sectors like office, retail and hotels will begin a slow recovery next year. Meanwhile industrial & logistics real estate and data centers will extend their rapid early recovery that is already underway, and multifamily will start its own swift rebound. All sectors will benefit from the widespread availability of a vaccine, a prospect that was enhanced by Pfizer’s November 9th announcement of a treatment that it says proved more than 90% effective in preliminary trials.

CBRE outlines in its new 2021 U.S. Real Estate Market Outlook that it expects interest rates will remain low, even as GDP rebounds by 4.5 percent next year. The spending plans of President-Elect Joe Biden will be moderated if the GOP retains control of the Senate after two run-off elections in early January. Elsewhere, the President-Elect’s plans could result in increased demand for health-care real estate and for properties tied to infrastructure and R&D.

“Overall, we expect the real estate recovery, particularly the office sector, to lag the broader economic recovery by several quarters. This follows the pattern of previous cycles but with the added complication of getting people back into the workplace,” said Richard Barkham, CBRE global chief economist and head of Americas research. “Two factors are essential for this recovery to take hold: a medical resolution to COVID-19 through a vaccine and other measures, and another fiscal stimulus package.”

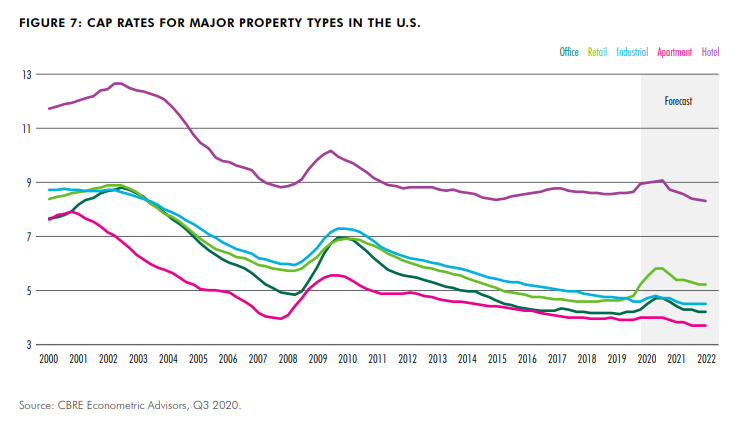

In Real Estate Capital Markets, CBRE expects that the improving economy, alongside aggressive Quantitative Easing by the Federal Reserve, will hold values stable and in some cases put downward pressure on capitalization rates. For now, there remains a wide gap between buyers seeking discounts and sellers not willing to offer them, but this will narrow over the course of the year. Investors have about $300 billion earmarked for real estate investment, much of it in North America.

CBRE’s report details the 2021 outlook for multiple sectors.

Industrial & Logistics

CBRE anticipates nearly 250 million sq. ft. of industrial & logistics space to be absorbed in 2021, more than the previous five-year annual average of 211 million sq. ft. Adaptive reuse of retail space for logistics uses will accelerate. Construction completions will rise by 29 percent in 2021 from 2020, and rents will continue to increase.

Multifamily

Suburban multifamily will outpace urban properties in the recovery. CBRE foresees U.S. multifamily returning to pre-pandemic occupancy levels in 2021 with rents fully recovering by 2022. Investment volume is projected to rise 33 percent in 2021 to $148 billion, still well short of the 2019 total of $191 billion.

Data Centers

CBRE forecasts data center inventory to increase by 13.8 percent in 2021. Hyperscale activity likely will level out next year as demand that surged in 2020 begins to plateau.

Office and Occupier

Office market fundamentals are expected to begin to recover in late 2021. Suburban office markets will recover more quickly, while downtown markets will pick up later in the year, as mass-transit commuting resumes. Whether suburban or urban, most companies will start to shift to a hybrid of in-office and remote work with the office as the primary base, CBRE surveys show. In addition, more companies will use flex space as they shift to more agile office occupancy strategies.

Hotels

Group and business travel will remain weak in 2021, meaning the overall hotel recovery will take several years. CBRE sees U.S. hotel occupancy slowly returning to pre-pandemic levels through 2023. Drive-to leisure destinations have already started to recover and will do well in 2021.

Retail

E-commerce sales growth will slow in 2021, and may even fall back a little, in the wake of the pandemic-related surge of 2020. Sales from brick-and-mortar retail will recover as economies reopen amid the eventual widespread availability of a COVID-19 vaccine and may even surprise on the upside on the back of post-COVID relief and pent up demand. Even so, CBRE predicts a 20 percent reduction in total U.S. retail square footage by 2025 from the current 56 sq. ft. per capita. Innovative private capital will lead investment in retail real estate while institutional capital will continue to pull back.

To download the full report, click here.