The recovery of the 12 largest U.S. office markets achieved the strongest momentum in the month of September since the onset of the pandemic, according to CBRE’s monthly “Pulse of Office Demand” report.

CBRE found that companies took advantage of favorable market conditions to lease space – especially the plentiful inventory of sublease space – at a faster pace. Many signed long-term leases, shifting away from the short-term renewals seen earlier in the pandemic.

To gauge the pace of recovery, CBRE’s monthly report tracks the three leading indicators of office market activity: tenants-in-the-market (TIM), which quantifies the amount of office space that companies are actively seeking; leasing activity in the form of finalized lease agreements; and the availability of sublease space.

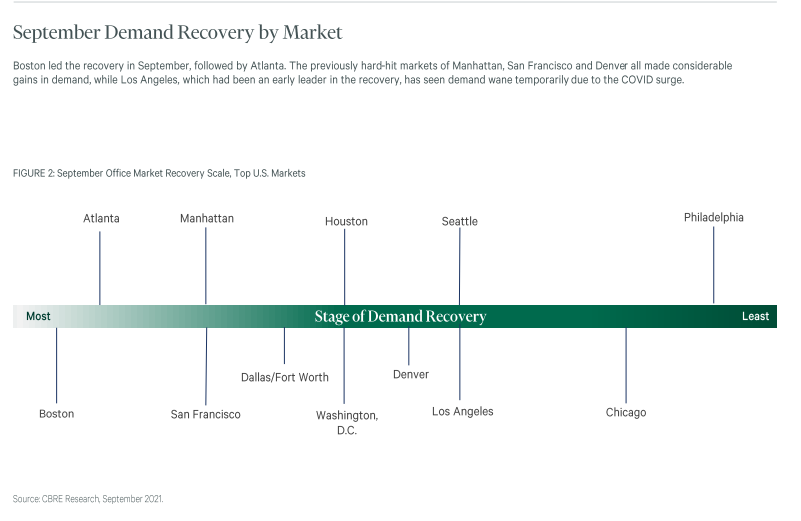

CBRE’s analysis of the indices based on September’s activity identified Boston as the top market for recovery, while demand in the Atlanta office market is also gaining strength. The previously hard-hit cities of Manhattan, San Francisco and Denver made considerable strides with improved demand, while Los Angeles, which had been an early beacon of recovery, suffered from depressed demand.

“With significant improvement in both the leasing and sublease indices, it appears that the top 12 U.S. office markets are indeed beginning to recover,” said Nicole LaRusso, CBRE Senior Director of Research & Analysis. “As the summer’s Covid surge fades into the distance, and vaccination rates continue to climb, we are cautiously optimistic that the improvement in office demand will build through the end of 2021 and into 2022.”

A national view of the indices reveals the progress of the office market’s recovery. For each index, a reading of 100 equates to the pre-pandemic levels of 2018 and 2019.

The Tenants-in-the-Market (TIM) Index was 83 in September, down one point from the August figure. The decline reflects the conversion of TIM activity to leases. Boston and San Francisco topped the list for tenants in the market, with both cities exceeding their pre-COVID baselines. San Francisco (108) has shown steady improvement in recent months, with its TIM index climbing to the second-highest place in the U.S. ranking. Manhattan (89) also gained considerably, growing 10 points month-over-month.

The Leasing Activity Index showed marked improvement in September, mitigating lingering concerns about the surge in infection levels last summer. The index jumped 17 points to 93, driven by a surge in leasing in Boston, where the index reached 210. Excluding Boston, the Leasing Activity Index gained 6 points to a level of 82. Nine of the 12 Pulse markets saw their indices increase in September. Atlanta (130) performed well ahead of its pre-pandemic baseline with a 28-point increase from August. Manhattan (95) also surged ahead in September, gaining 31 points over the August level.

The Sublease Availability Index provided another signal of recovery, dropping ten points to 181. This marked the third consecutive monthly decline since the index peaked in June at 195. The improvement is accelerating as companies seize well-priced, built-out space offered on the sublease market. Sublease availability improved in 10 of the 12 Pulse markets in September. Atlanta (161) and Philadelphia (180) each saw their indices fall by over 30 points. Denver (181) was down 21 points, while San Francisco (319) and Boston (145) were down 18 and 17 points, respectively. Seattle’s level fell by 10 points to 251.

“The pandemic has taught us all that it’s best to keep optimism cautious. That said, September’s indices for office-leasing activity are encouraging by nearly any measure,” said Julie Whelan, CBRE Global Head of Occupier Research. “This should set the foundation for continued recovery, absent any unforeseen shocks.”

To read the full report, click here.