The possible WeWork IPO has put flexible-office space front and center. In May, WeWork reported $728.43 million in Q1 2019 revenue, but it also showed $264 million of net loss. That loss is a slight improvement over $274 million in Q1 2018. The year-over-year membership rose from 220,000 to 466,000.

From CBRE’s MarketFlash report:

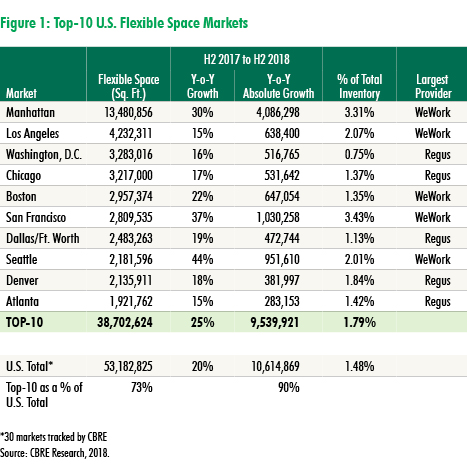

“While questions have been raised about the profitability of these operators in a recession, it is unquestionable that the meteoric growth of the flexible-space sector is unprecedented in commercial real estate. Here is what we know about the (flexible space) sector today (based on the 30 markets tracked by CBRE):

- The top-10 markets account for more than 70% of the nation’s flexible-office inventory (25% in Manhattan alone). With nearly 4 billion sq. ft. of traditional office space in the 54 major metros tracked by CBRE, continued growth of flexible space is inevitable even under conservative estimates.

- In 2018 alone, flexible space in the top-10 markets grew by 25%, with Manhattan growing the most on an absolute basis (+4 million sq. ft.) and Seattle growing the most on a percentage basis (44%). Growth since the start of this cycle has been constant and is showing no signs of slowing. Flexible-space operators are currently in the market for more than 6 million sq. ft. of space.

- Flexible space as a percentage of total office inventory is around 2%, with San Francisco and Manhattan being the most saturated (over 3% each). In some foreign markets, such as London and Beijing, flex space accounts for more than 5% of total office inventory.

- Only 15 markets have more than 1 million sq. ft. of flexible-office inventory. Many U.S. markets have not even scratched the surface of this sector, including high office-using employment growth markets like Nashville, Austin and Charlotte.

- The top-five operators by square footage are WeWork, Regus, Spaces, Knotel and Industrious. The We Company (WeWork) and IWG (Regus and Spaces) hold 50% of the U.S. flexible-office inventory. Knotel and Industrious have another 10%.

- The Fortune 500 is engaged and intrigued. 85% of real estate executives plan to implement flexible-office solutions into their portfolio strategy, according to the 2018 Americas Occupier Survey. Enterprise customers are early in the implementation stage of flexible-office solutions as a portfolio strategy. If these strategies prove successful, there is potential for more explosive growth of coworking.l office market because of the value they provide to a broad range of occupiers.”